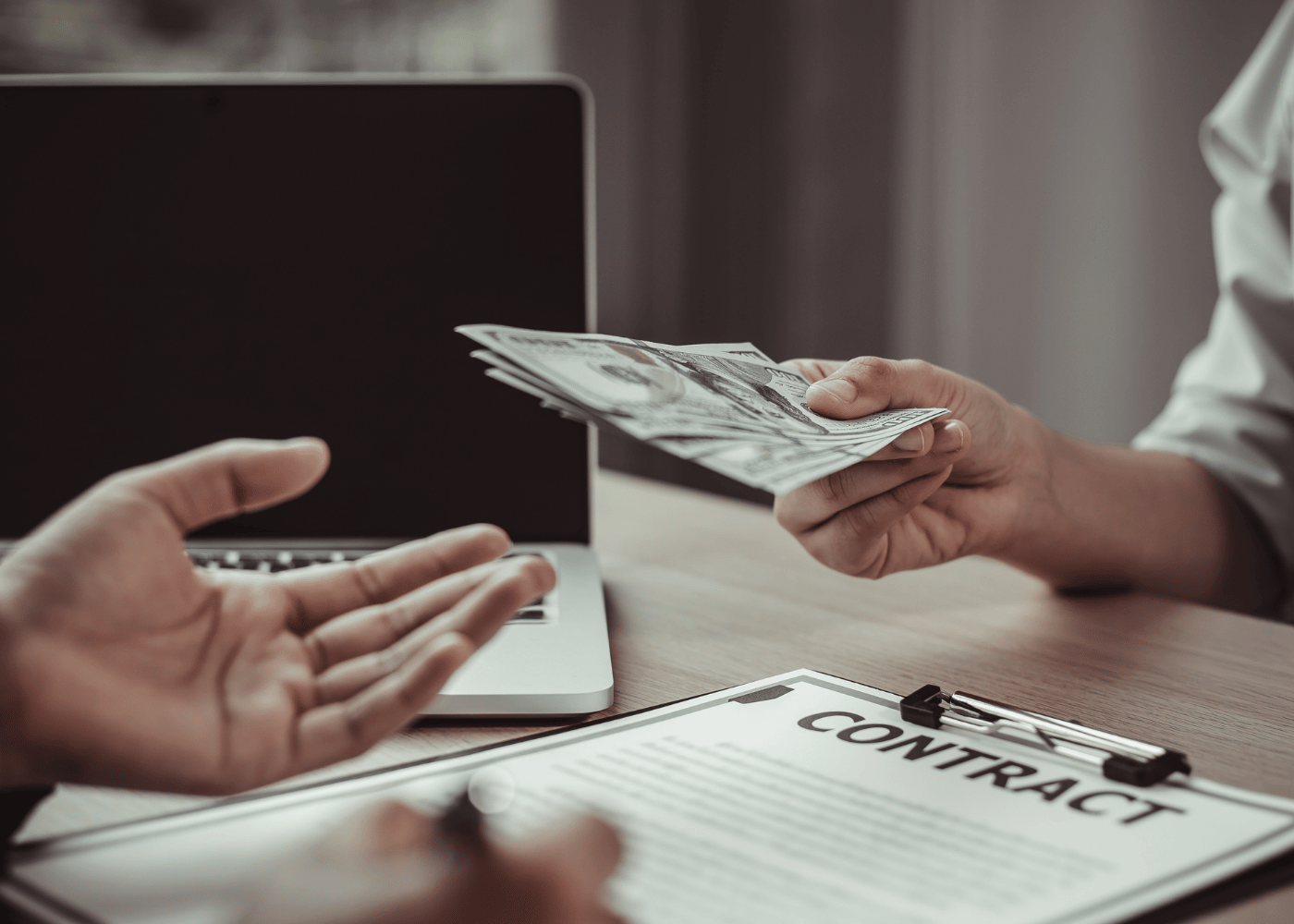

Inside the Atlanta Hawks fraud: How one executive exposed the cost of complacency A $3.8 million fraud at the Atlanta Hawks shows how weak controls and unchecked access can bring any organisation down. Nick Henderson-Mayo November 11, 2025

One in 35 UK businesses faced bribery last year: Inside the Economic Crime Survey 2024 The Economic Crime Survey 2024 reveals rising fraud, bribery and money laundering risks, many now cyber-enabled | Here's what you need to know Sara Henna Dahan November 6, 2025

HMRC deals the first CCO prosecution just as ‘Failure to Prevent Fraud’ kicks in HMRC’s first CCO prosecution, Bennett Verby, arrives just as FTPF goes live. Are your reasonable procedures defensible? Sara Henna Dahan September 17, 2025

Compliance Training, Corporate fraud, Failure to Prevent Fraud, Fraud Prevention Training, Fraud Training Failure to Prevent Fraud: 40% of Companies Haven’t Trained Staff, VinciWorks Poll Finds A new VinciWorks poll reveals 4 in 10 UK companies haven’t trained staff on the Failure to Prevent Fraud offence. Learn why this training gap could expose your business to criminal liability and how to fix it. Asha Purohit September 16, 2025

Failure to prevent fraud in Scotland: The Procurator Fiscal’s distinct approach What does the updated guidance from the Procurator Fiscal say about prosecuting failure to prevent fraud offences in Scotland? Nick Henderson-Mayo September 3, 2025

Transatlantic corporate crime: How the UK and US will investigate and prosecute cases together UK–US guidance signals joint action on tariff evasion and tax fraud—companies must tighten compliance for cross-border prosecutions. Nick Henderson-Mayo August 27, 2025

Corporate fraud, CPS, SFO UK corporate prosecutions: What the new guidance means for businesses UK corporate prosecutions: What the new guidance means for businesses. The UK’s corporate crime landscape is undergoing a huge change. Naomi Grossman August 26, 2025

Could a family law case trigger a failure to prevent fraud investigation? How deliberate asset concealment in family law could trigger fraud, AML, and Failure to Prevent Fraud investigations under UK law and ECCTA. Nick Henderson-Mayo August 11, 2025

PSD3 gets real: What the EU’s new payment rules mean for you Get up to speed on PSD3 and PSR, the EU’s new payment and fraud rules, and learn how to prepare for the UK’s failure to prevent fraud offence. Sara Henna Dahan August 6, 2025