Equality Act, Inclusion, leadership, micro-behaviours, protected characteristics, race, recruitment, teamwork, unconscious bias Understanding and tackling race bias: Managers’ guide VinciWorks September 7, 2022

body language, communication, Inclusion, micro-affirmations, micro-aggressions, micro-behaviours, micro-inequities, motivation, relationships, unconscious bias The impact of micro-behaviours VinciWorks September 7, 2022

Flexible Working, gender bias, job advert, recruitment, sex discrimination, Social Media, unconscious bias Understanding and tackling gender bias VinciWorks September 7, 2022

mentoring, micro-behaviours, performance appraisals, recruitment, unconscious bias Understanding unconscious bias VinciWorks September 7, 2022

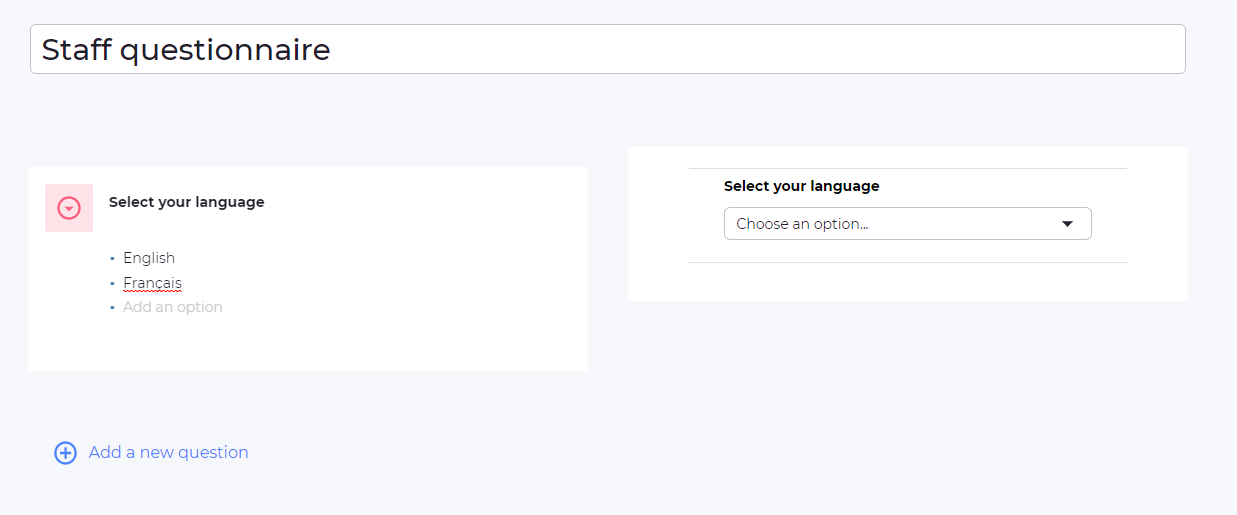

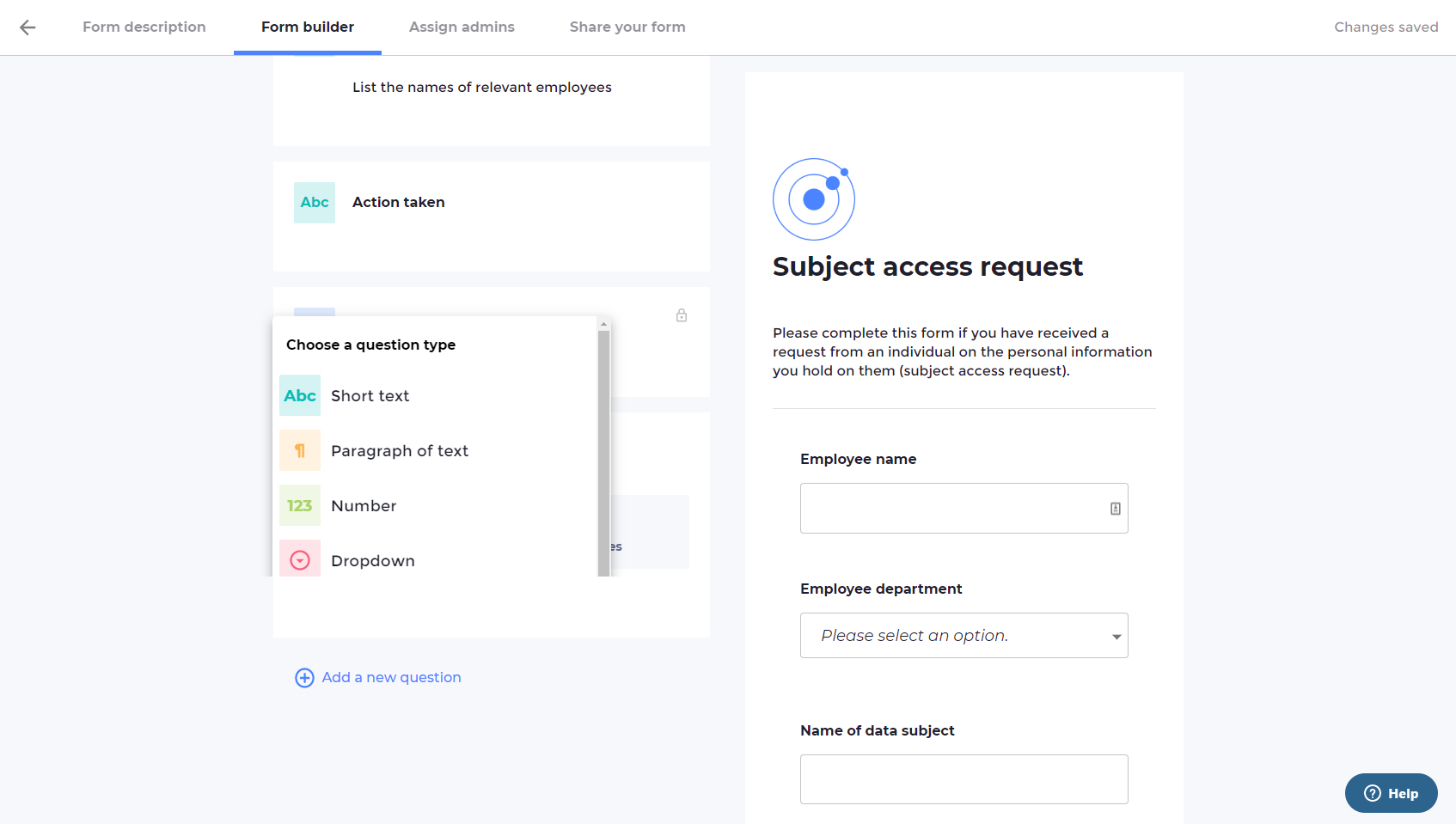

Omnitrack: How to use conditional descriptions to provide your form in multiple languages With Omnitrack’s versatile conditional logic, you can easily build each language into the form. VinciWorks September 7, 2022

aspiring leaders, communication, influence, influencing, leadership, persuasion, story-telling Influencing people VinciWorks September 6, 2022

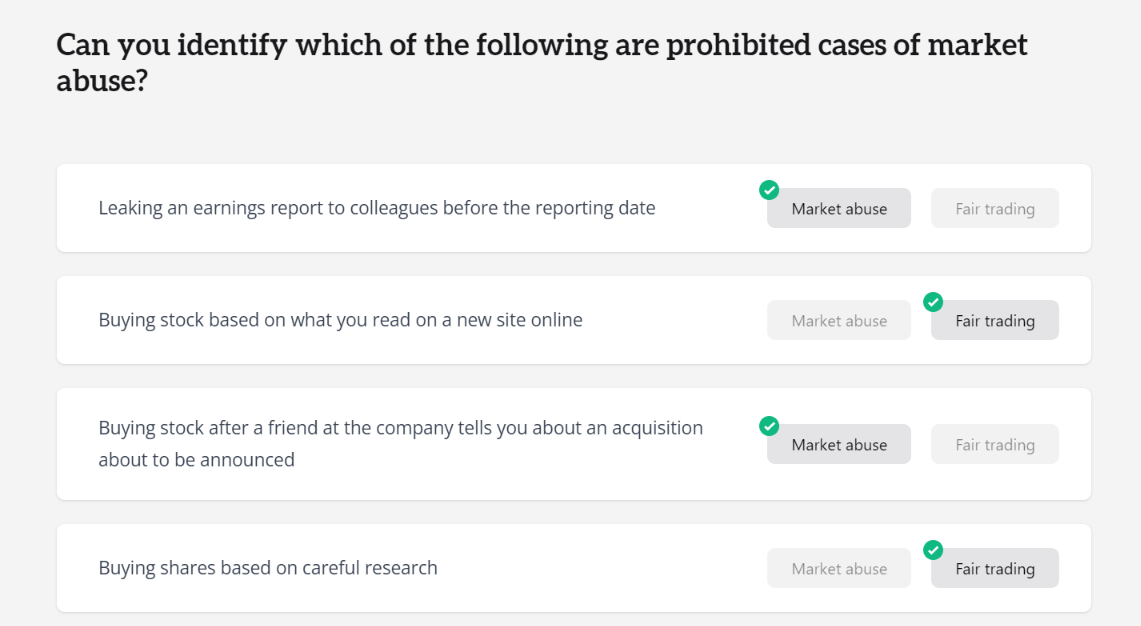

Upcoming course release: Fraud and Market Abuse VinciWorks' new course Fraud & Market Abuse - Fundamental concepts trains staff on the concepts and rules of market abuse and fraud. VinciWorks September 6, 2022