UK announces major changes to the Money Laundering Regulations – what do they include? What's included in the UK government's statutory instrument to amend the Money Laundering Regulations 2017? Download our guide. Nick Henderson-Mayo September 9, 2025

Solicitor disciplined over Azerbaijani funds: SDT exposes long shadow of AML failures The Solicitors Disciplinary Tribunal has fined and sanctioned Rory Fordyce for AML failures linked to Azerbaijani Laundromat scandal. Nick Henderson-Mayo August 4, 2025

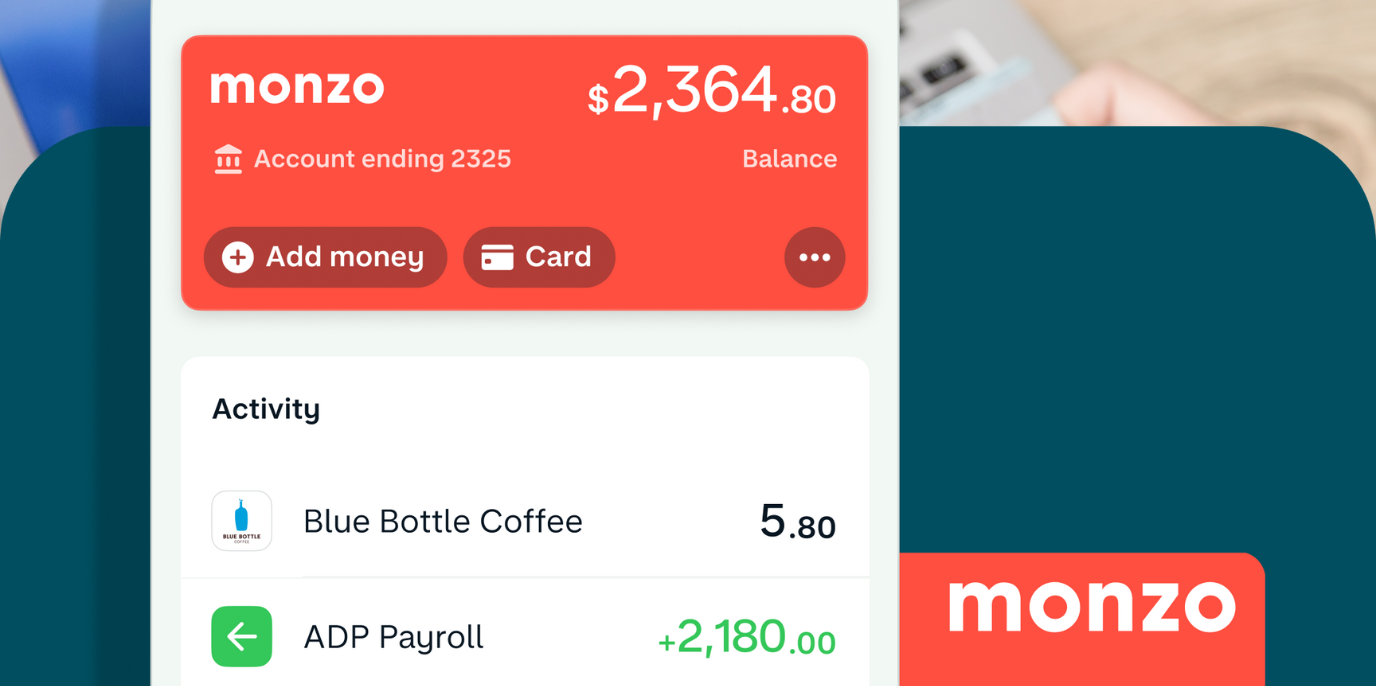

Slick app, sloppy controls: The £21M AML fine that caught up with Monzo Monzo’s £21M fine shows how fast growth without strong AML controls can lead to serious risk and regulatory fallout. Sara Henna Dahan July 14, 2025

The UK’s overseas territories are failing on dirty money: What now? British overseas territories missed a key transparency deadline. What does this mean for UK anti-corruption efforts and compliance risk? Sara Henna Dahan July 8, 2025

Is your VC ready for the new US AML rules from 1 January 2026? Starting January 2026, VC and private equity firms must comply with FinCEN's AML regulations under the Bank Secrecy Act. Is your firm ready? Nick Henderson-Mayo June 22, 2025

June 2025 FATF Grey List updates – guide to high risk jurisdictions What countries were added and removed to the FATF Grey List in June 2025? Bolivia and Britiish Virgin Islands are now high risk for AML Nick Henderson-Mayo June 19, 2025

£120,000 fine for Southend law firm over long-term AML failures is a stark lesson in the importance of AML risk assessments Southend law firm Tolhurst Fisher was fined £120,000 for failing to conduct an AML risk assessment | Learn how to avoid the same mistake Sara Henna Dahan May 19, 2025

TD Bank’s recent AML leadership overhaul is a wakeup call for the financial services sector After a record $3B fine, TD Bank is overhauling its AML team. What went wrong, and what are the implications for AML compliance? Sara Henna Dahan May 5, 2025

Yorkshire law firm fined £36K for anti-money laundering failures Holden Smith Law was fined £36,000 for anti-money laundering breaches. What went wrong and how can firms avoid similar pitfalls? Sara Henna Dahan April 23, 2025