What is Professional Liability Insurance (PII)?

Professional liability insurance, also known as errors and omissions (E&O) insurance, is a type of coverage that protects professionals and organisations from liability claims arising from their professional services or advice. It provides financial protection for legal defence costs, settlements, or judgments if a client alleges that the professional’s actions, advice, or negligence caused financial loss or harm. This insurance is essential for professionals across various fields, including medicine, law, accounting, architecture, engineering, consulting, real estate, and technology, as it safeguards their assets and reputation from the potential financial consequences of lawsuits or claims related to errors, omissions, negligence, or breaches of duty in their work.

What does Professional Liability Insurance cover?

Professional Indemnity Insurance (PII) covers organisations for compensation claims made by clients or other third parties. The FCA explains:

“Professional indemnity insurance (PII) is liability insurance that covers firms when a third party claims to have suffered a loss, usually due to professional negligence.”

Professional Liability Insurance typically covers the following aspects: Professional Negligence, Legal Defence Costs, Errors and Omissions, Breach of Confidentiality, Libel or Slander, and Legal/Regulatory Compliance.

Why do FCA firms need Professional Liability Insurance?

FCA (Financial Conduct Authority) firms require Professional Liability Insurance for several reasons:

Regulatory Compliance: The FCA mandates that certain regulated firms, such as investment firms, insurance brokers, and financial advisors, maintain Professional Indemnity Insurance (PII) as a part of their regulatory obligations

Client Protection: Professional Liability Insurance provides a safeguard for clients or customers who may suffer financial loss or harm due to the actions or advice of an FCA-regulated firm

Risk Mitigation: Professional Liability Insurance helps mitigate the financial risks associated with potential claims and legal proceedings

Business Continuity: In the event of a professional liability claim, having appropriate insurance coverage helps FCA firms to manage the financial impact without jeopardising their business operations

Market Confidence: The requirement for Professional Liability Insurance enhances market confidence by instilling trust and credibility in the financial services industry

FCA Regulatory Oversight: The FCA maintains oversight and supervision of regulated firms to ensure compliance with regulatory standards

How to obtain Professional Liability Insurance(PII)

In order to obtain insurance, someone with sufficient seniority at an FCA-regulated firm (e.g. a principal, partner or director) would normally begin by completing a form for an insurance broker. The form will then be used by the insurer to calculate the cost of the premium. Some of that information should be readily available to the person submitting the form, such as the type of services the firm provides, as well as its overall income.

However, there are questions that are used to calculate a firm’s risk profile that a senior manager may not be able to answer immediately. That is because the answers to these questions will be based on information spread throughout the firm, rather than held by any one individual. There are practical challenges in collecting such information from employees, which we will address below. But first, we will look closer at PII as it applies to financial service firms.

PII – What are the challenges for FCA-regulated firms?

PII is not unique to those providing financial services and is also typically taken out by other professionals, such as law firms. However, there are certain challenges when it comes to taking out PII which are particular to FCA-regulated firms. This is because the risks relating to the services offered by a financial services firm may require a specialist insurer. Even specialist insurers will inevitably ask generic questions in the proposal form, such as those relating to the amount of revenue your organisation makes. But there are also likely to be specific questions related to financial services. For example, insurers may wish to know whether any employees offer your clients advice and, if so, whether that advice is independent or restricted, as this could affect your risk profile.

In addition to your insurer’s requirements, you should also be aware of your obligations towards the FCA. For instance, the FCA Handbook sets out rules for firms carrying on certain activities, including insurance distribution and home finance mediation. This chapter includes the PII requirements for relevant firms, such as the terms to be incorporated and the minimum limits of indemnity.

For example, if you are an insurance intermediary, the minimum limit of indemnity per year for a single claim is €1,300,380. The minimum aggregate limit of all claims must be the higher of: €1,924,560 and 10% of your firm’s annual income (up to £30 million).

How can VinciWorks help?

The Omnitrack FCA Compliance Suite now includes a PII Trawling form, which helps you collate the information you need to compile a successful insurance application.

- Customisation: Insurers will look at different factors to create a risk profile, depending on their own requirements, the size and complexity of your firm, and the services you provide. We can work with you to adapt the workflow, to ensure your staff are asked the right questions.

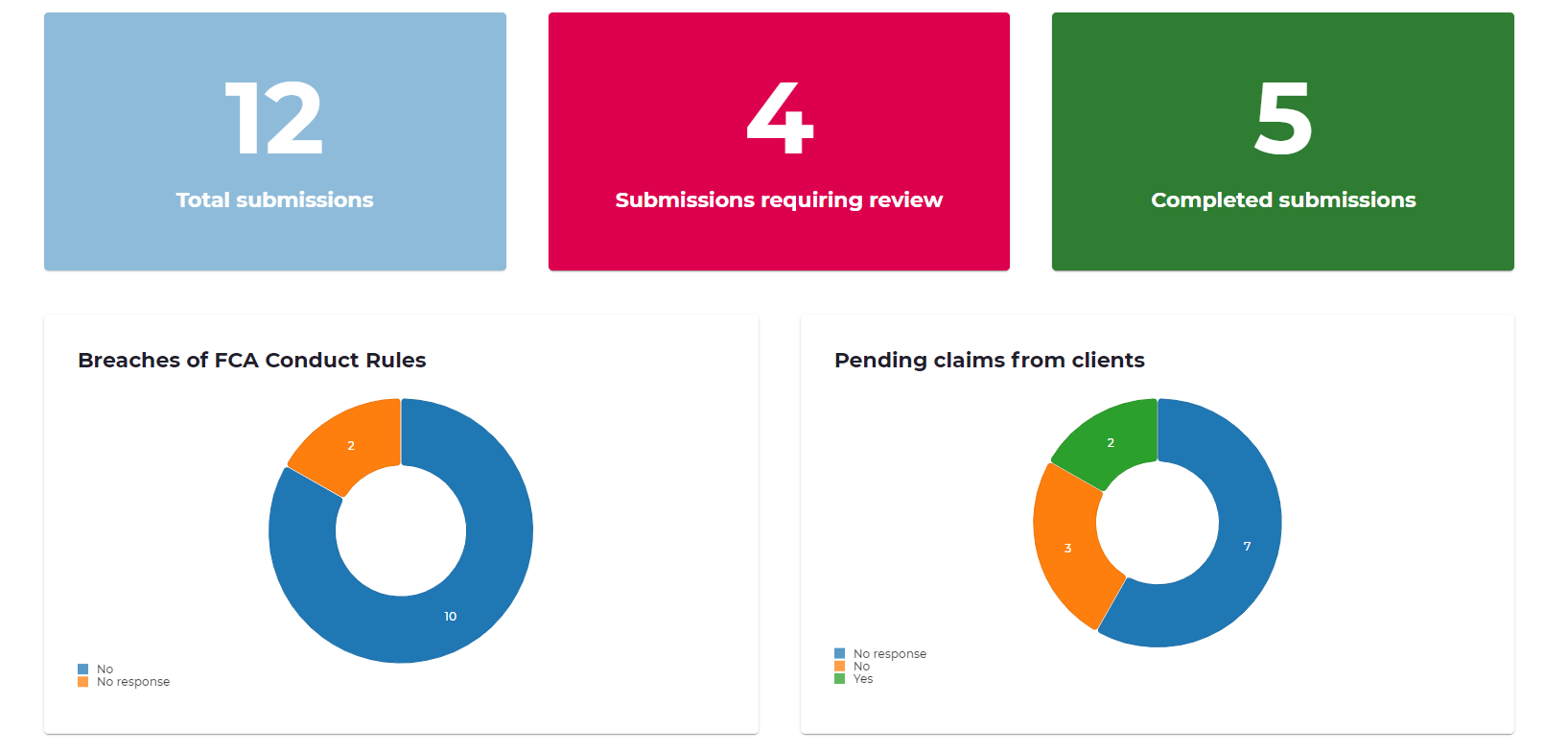

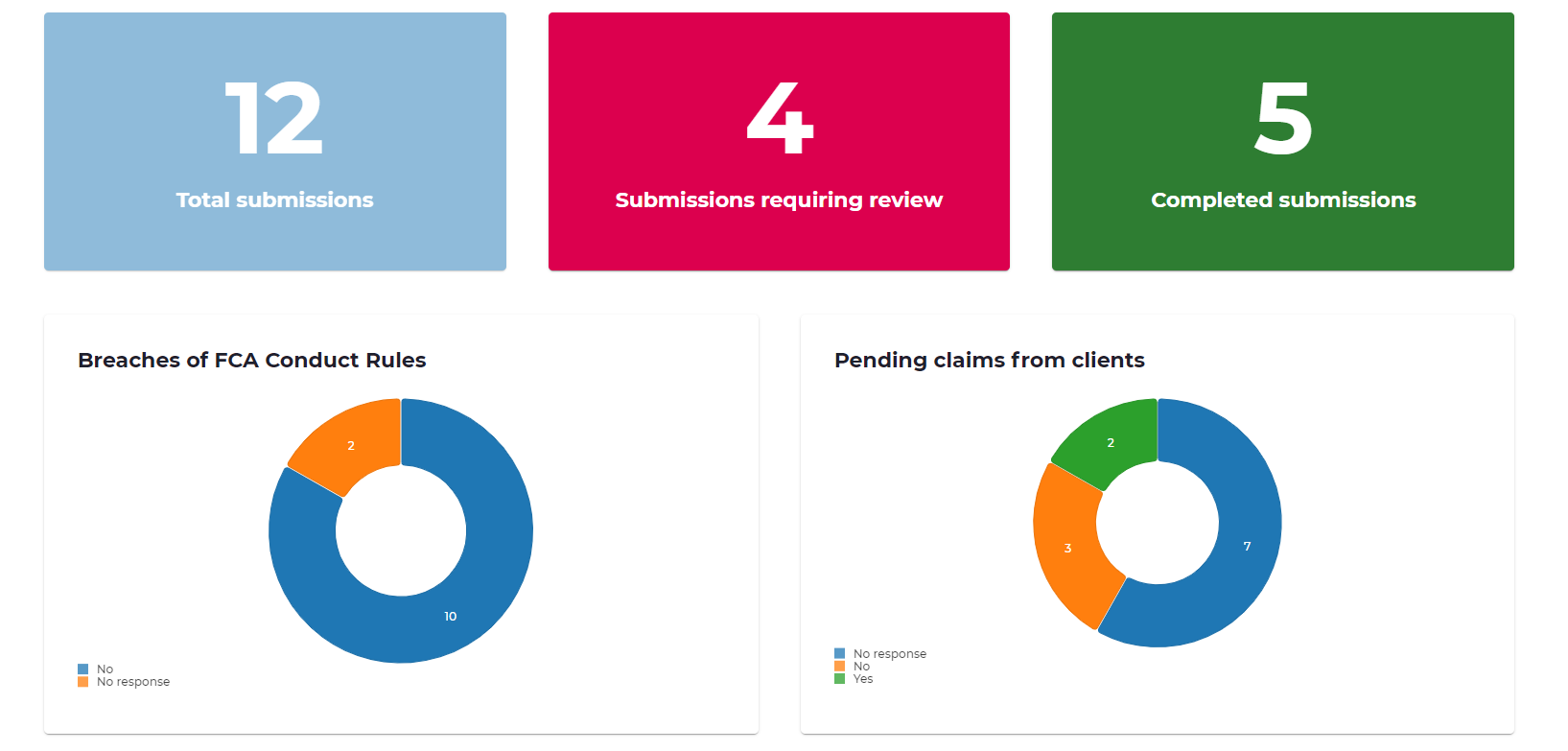

- Graphical dashboard: The customisable dashboard allows you to spot trends across all submissions. This allows you to address issues that could adversely affect your firm’s risk profile, such as training gaps, or staff who lack supervision.

- Reminder function: Custom rules can be created to generate reminders, ensuring your initial insurance application – and any renewals – are on schedule.

- Part of an FCA Suite: Use information from the PII form to populate other workflows. For example, if an employee identifies a breach of the FCA rules, this will be relevant for your insurance application, but can also be entered into the Incidents & Breaches register.

Depending on the financial services you provide, there may only be a limited number of specialist insurers who provide PII for the risks your firm faces. It is therefore important to complete an application that provides a comprehensive overview of your risk profile. Omnitrack enables you to check that your compliance systems are being followed by all staff, that employees are aware of your AML policy, the level of training staff have received over the last 12 months, and more. This gives you an understanding of your firm’s risk profile, helping you provide insurers with a strong application.