South Asia faces significant AML risks due to corruption, informal financial systems, and weak regulatory enforcement in several countries. The region’s large cash-based economies, extensive use of hawala networks for remittances, and vulnerabilities in trade-based money laundering make it particularly susceptible to illicit financial flows.

Key AML threats include terrorist financing, drug trafficking, and organised crime, which exploit gaps in beneficial ownership transparency and customer due diligence. While some countries, such as India and Pakistan, have made strides in aligning with FATF standards, enforcement remains inconsistent, particularly in cross-border transactions and informal markets.

The region also faces challenges related to political instability, cybercrime, and the growing adoption of cryptocurrencies, which complicates regulatory oversight. Since there are only six countries in the South Asia region, they are all included here.

Understanding national money laundering risks

Money laundering risks refer to the vulnerabilities within a country’s systems that criminals can exploit to integrate illicit financial gains into the legitimate economy. These risks stem from systemic weaknesses such as insufficient legal frameworks, corruption, lack of transparency, ineffective enforcement measures such as a weak police or judiciary, and political corruption.

At its core, money laundering enables crimes ranging from drug trafficking and fraud to terrorism financing. The interconnected nature of global financial systems means that these risks often transcend borders, impacting not just individual countries but the global economy at large.

Risks in one country can easily spill over into connected jurisdictions, as criminals exploit weaker systems to hide the profits of criminal enterprise into the legitimate economy. It is important for any firm which has the potential to be exploited for money laundering to understand the risks for each jurisdiction linked to transactions or clients they work with.

How should money laundering risks be categorised?

The Basel AML index provides a holistic view of country risks. It categorises risks based on five different areas, with different weighting given to each:

Quality of AML/CFT/CPF framework (50%): This includes compliance with international standards such as the Financial Action Task Force (FATF) Recommendations. Factors assessed include customer due diligence, reporting suspicious transactions, and the implementation of financial sanctions.

Corruption and fraud risks (17.5%): Transparency International’s Corruption Perceptions Index and indicators of financial crimes and cybercrimes provide a snapshot of the level of corruption and fraud in a jurisdiction.

Financial transparency and standards (17.5%): Indicators like the Financial Secrecy Index assess the openness of financial systems and the risk of financial institutions being exploited for illicit purposes.

Public transparency and accountability (5%): This domain evaluates public access to budget information, transparency of political financing, and accountability mechanisms in public institutions.

Political and legal risks (10%): Key indicators include judicial independence, the rule of law, media freedom, and political rights. Weaknesses in these areas can significantly exacerbate money laundering risks.

To measure a country’s risk level, the Basel AML Index uses a composite scoring methodology that integrates data from 17 publicly accessible indicators. These scores are summarised on a scale from 0 to 10, where 10 represents the highest risk.

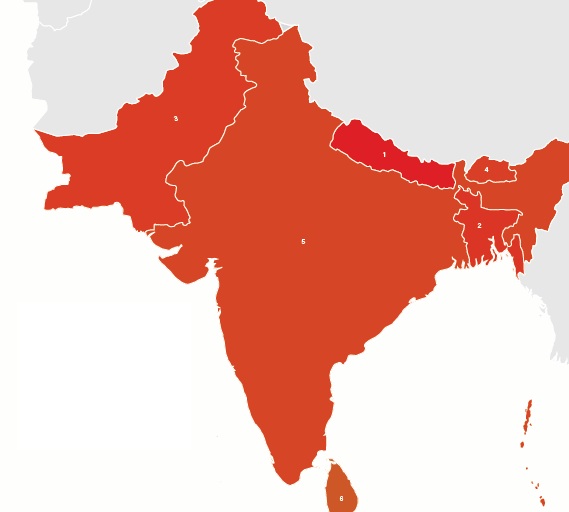

The highest risk countries in South Asia for money laundering

Nepal (Score: 6.01)

Nepal faces serious AML risks, driven by its cash-based economy, weak regulatory enforcement, and geographic proximity to high-risk regions. The country’s porous borders with India and China make it vulnerable to cross-border smuggling, drug trafficking, and informal remittance systems such as hawala. Nepal also struggles with terrorist financing risks, particularly as a potential transit point for funds linked to militant groups operating in South Asia. While Nepal has made efforts to align with FATF standards, gaps in customer due diligence, beneficial ownership transparency, and suspicious transaction reporting persist. Proliferation financing risks, though less pronounced, are exacerbated by weak monitoring of trade-based transactions and limited capacity for enforcement.

Bangladesh (Score: 5.62)

Bangladesh faces significant AML risks, primarily due to corruption, informal financial networks, and terrorist financing vulnerabilities. The country has been identified as a source of terrorist funding, particularly in connection with extremist groups operating domestically and across borders. Bangladesh’s reliance on remittances and hawala systems poses additional challenges in tracking illicit financial flows. While the government has made strides in strengthening AML frameworks and financial intelligence unit, enforcement remains inconsistent, and trade-based money laundering continues to be a major concern. Proliferation financing risks are also present, particularly given Bangladesh’s growing industrial sector and trade networks, which require enhanced oversight to monitor dual-use goods and prevent misuse for weapons proliferation.

Pakistan (Score: 5.56)

Pakistan has faced heightened AML/CTF concerns, leading to its inclusion on the FATF grey list from 2018 to 2022. While Pakistan has since improved its AML/CTF framework and exited the grey list, it remains vulnerable to terrorist financing due to the presence of militant groups operating within its borders. Weak enforcement, particularly in monitoring charities, religious institutions, and cash-based economies, has contributed to ongoing risks. Pakistan also faces proliferation financing risks, as it is a nuclear-armed state with sensitive technologies and materials requiring strict oversight. Although Pakistan has implemented reforms to track cross-border financial flows and strengthen beneficial ownership transparency, enforcement gaps and the influence of informal remittance systems like hawala remain key challenges.

Bhutan (Score: 5.51)

Bhutan is considered a lower-risk jurisdiction in South Asia but still faces AML vulnerabilities due to its cash-based economy and limited regulatory resources. The country’s geographic location near major trade routes makes it susceptible to trade-based money laundering and smuggling. While Bhutan has taken steps to strengthen its AML framework, including aligning with FATF standards, enforcement remains limited, particularly in customer due diligence and beneficial ownership transparency. Bhutan’s terrorist financing risks are relatively low due to its stable political environment, but it faces potential proliferation financing risks linked to trade with higher-risk countries, necessitating ongoing monitoring and oversight.

India (Score: 5.49)

India is a major financial hub in South Asia and faces moderate AML risks despite its strong regulatory framework. The country’s large and diverse economy makes it vulnerable to trade-based money laundering, tax evasion, and hawala transactions. India also faces terrorist financing risks, particularly linked to cross-border terrorism originating from neighbouring countries. The government has taken steps to strengthen AML and CTF frameworks, including improving financial intelligence capabilities and introducing stricter reporting requirements for financial institutions. However, proliferation financing risks remain a concern, especially in sectors like defence and technology exports. India’s enforcement mechanisms are improving, but challenges persist in addressing informal financial networks and cross-border illicit flows.

Sri Lanka (Score: 5.28)

Sri Lanka faces moderate AML risks, particularly due to its history of terrorist financing associated with the Liberation Tigers of Tamil Eelam (LTTE). While the LTTE has been dismantled, concerns persist about residual networks and illicit financial flows through remittances and charitable donations. The country’s reliance on cash-based transactions and informal financial systems also makes it vulnerable to money laundering and trade-based schemes. Proliferation financing risks are lower, but weaknesses in border controls and trade monitoring pose challenges. Sri Lanka has strengthened its AML framework in recent years and exited the FATF grey list in 2019, but enforcement gaps and capacity constraints remain issues requiring continued focus.